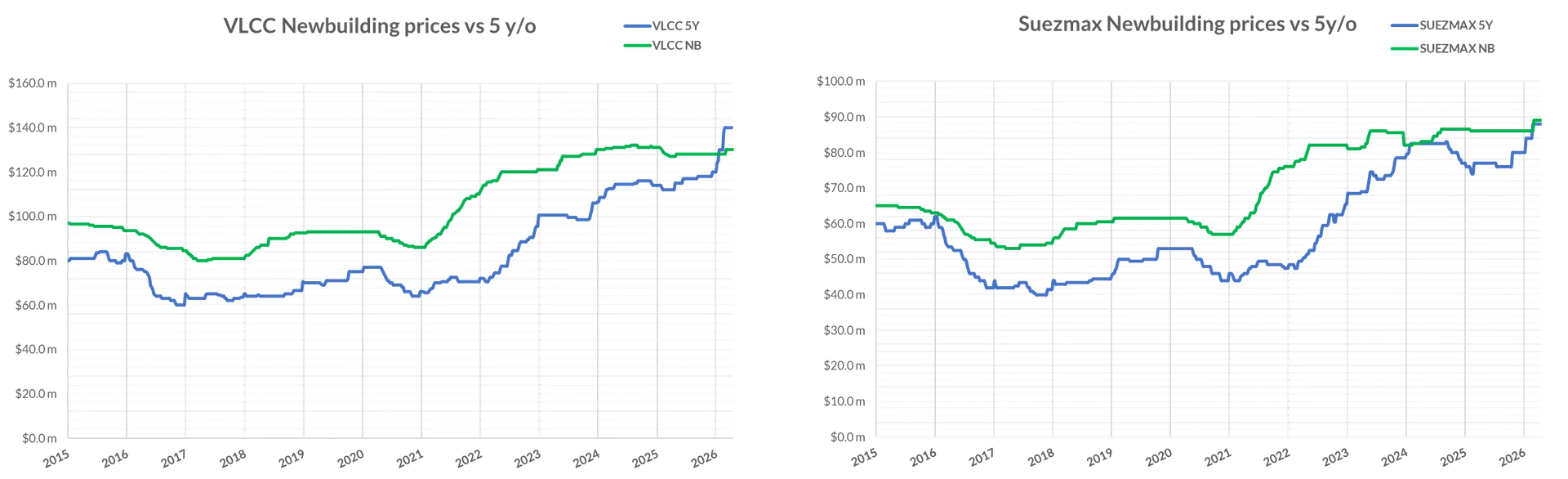

Newbuilding activity has shifted into a clear dirty tanker ordering spree, with owners concentrating on large crude capacity while yard pricing continues to move higher. March recorded 92 newbuilding contracts across tankers and bulkers, including 67 tankers, with disclosed firm pricing of about $3.64bn and more than 70% of that capital directed to VLCCs and Suezmaxes.

Suezmaxes led by volume at 25 units, followed by 17 VLCCs, while MRs accounted for 18 units but only 2.5% of disclosed capital, keeping the financial weight firmly with crude. The pricing signal has tightened further, with a five year old VLCC reported above newbuilding price and the five year old Suezmax now close to parity.

April ordering has extended the pattern, with reported VLCC business including Mercuria at DSIC, Advantage Tankers at DSIC, JP Morgan linked VLCCs at DSIC, and Harry Vafias at Hanwha Ocean, while Yangzijiang Maritime Development entered the VLCC market with eight 319,000 dwt newbuildings for 2028 to 2030 delivery.

Capesize average earnings were $37,500/day with the BCI up 24.5% w o w to 4,130. Panamax average earnings were $17,800/day with the BPI up 6.5% w o w to 1,975. Supramax average earnings were $17,900/day with the BSI up 8.2% w o w to 1,415. Handysize average earnings were $13,300/day with the BHI up 6% w o w to 741.

Capesize tightened on South Brazil and West Africa to China, with C3 in the low $32s per ton and a 175,000 dwt fixed Tubarao with West Africa option to Qingdao at $30.8 per ton.

Panamax improved on firmer grain and fronthaul demand, with an 82,000 dwt fixed delivery Barcelona via NCSA redelivery Singapore Japan at $23,000/day.

Supramax improved in the US Gulf, with a 63,000 dwt fixed in the low $30,000s/day for a transatlantic run.

Handysize stayed mixed with the Continent and Mediterranean subdued, with a 37,000 dwt fixed US Gulf with scrap redelivery Peru at $12,500/day.

Capesize strengthened on sustained miner enquiry and tighter prompt tonnage, with C5 in the mid $13s per ton and a 181,000 dwt fixed delivery North China for an intra Pacific trip at $31,500/day.

Panamax held a better tone on healthier cargo flow and tighter prompt supply, with an 82,700 dwt fixed delivery Lianyungang via NoPac redelivery Singapore Japan at $15,000/day.

Supramax advanced on steadier cargo flow and tighter tonnage, with a 57,000 dwt fixed delivery North China redelivery South Africa at $18,000/day.

Handysize improved as prompt tonnage stayed tight, with a 37,000 dwt fixed delivery West Australia redelivery China in the $17,000s/day.

VLCC was mixed, with TD15 West Africa to China firm at $110,000/day and US Gulf to China indicated around $16.55m.

Suezmax softened, with TD20 West Africa to Continent at $82,300/day and TD27 Guyana to UK Continent at $80,300/day on limited enquiry and ample tonnage.

Aframax corrected from prior highs but stayed very firm, with TD25 US Gulf to Continent at $91,200/day and TD26 East Coast Mexico to US Gulf at $130,500/day.

LR firmed in the Atlantic, with LR2 TC20 ME Gulf to UK Continent rising to $141,700/day.

MR lost momentum in the Atlantic, with TC21 US Gulf to Caribs at $104,700/day and TC2 Continent to US Atlantic Coast at $28,500/day.

VLCC softened in the MEG, with TD3C ME Gulf to China at $431,200/day as Hormuz transits remained limited.

Suezmax opportunities East of Suez stayed restricted, with owners watching whether any easing in Hormuz constraints translates into activity.

Aframax in the Mediterranean eased, with TD19 cross Med at $106,400/day as owners looked for a floor on limited enquiry.

LR stayed firm East of Suez, with LR2 TC1 ME Gulf to Japan at $157,900/day and LR1 TC5 ME Gulf to Japan at $129,300/day.

MR firmed in the Pacific, with TC7 Singapore to East Coast Australia at $45,000/day.

Over the past twelve months, Greek interests remained the leading sellers with 325 vessels across sectors, versus 149 sales by Chinese sellers, with Greek selling led by 154 dry bulk and 122 tankers and Chinese selling led by 97 dry bulk and 33 tankers.

On the buying side, China ranked first with 224 purchases and Greece followed with 219, with Chinese buying led by 170 dry bulk and Greek buying led by 115 dry bulk alongside 76 tankers.

This post provides a high-level view of crude tanker ordering trends, newbuilding momentum, and current freight market performance.

The full Allied QuantumSea Weekly Market Report – Week 16 includes:

In-depth analysis of dirty tanker ordering activity and crude capacity expansion

Detailed newbuilding trends across VLCC, Suezmax and MR segments

Pricing comparisons between secondhand and newbuilding tanker values

Dry bulk and tanker earnings tables across all vessel classes

Atlantic & Pacific route-level freight analysis with fixture benchmarks

Baltic indices, TCE calculations & historical performance comparisons

Secondhand S&P transactions, buyer–seller positioning & asset value trends

Recycling activity and scrap pricing indicators

👉 Fill in the form below to subscribe and receive the complete PDF directly in your inbox every week.