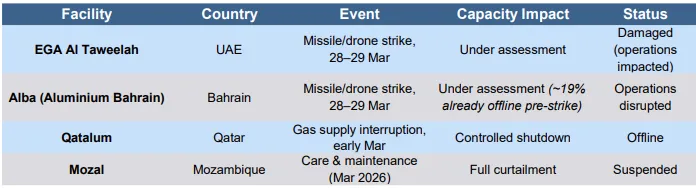

Strikes at key Gulf smelters together with disruption around Hormuz are tightening aluminium supply and adding pressure across freight and logistics. Aluminium prices have moved back to levels last seen during the previous major tightness, with exchange stocks drawn down, the forward curve pointing to near term tightness, and physical premiums in the United States and Europe higher.

The latest strikes hit two major Gulf smelters alongside other curtailments already in place, leaving a meaningful share of regional capacity either offline or disrupted and reducing system flexibility. Handy and Supramax appear among the most exposed dry bulk classes given their role in moving alumina and aluminium products from Gulf ports, while disruption is adding repositioning pressure, idle time and longer ballast legs, and container flows to the United States and Europe are facing rerouting, booking disruption and war risk surcharges.

The near term picture depends on the extent of damage at EGA and Alba, the geopolitical path, and whether commercial navigation through Hormuz becomes more reliable, with the risk of a larger aluminium shortfall rising if current disruption proves prolonged.

Dry Bulk Analysis – Week 13 2026

Capesize average earnings were $27,500/day with the BCI up 2% w o w to 3,032. Panamax average earnings were $15,800/day with the BPI down 7.8% w o w to 1,756.

Supramax average earnings were $15,200/day with the BSI down 1.5% w o w to 1,206. Handysize average earnings were $12,800/day with the BHI down 4.2% w o w to 713.

Dry Atlantic Analysis – Week 13 2026

Capesize strengthened, with C3 Brazil and West Africa to China moving into the mid to high $30s per ton and a 175,000 dwt fixed Tubarao with a West Africa option to Qingdao at $30.75/ton.

Panamax stayed under pressure as transatlantic and fronthaul remained subdued, with an 82,800 dwt fixed delivery Brest for a trip via NC South America with redelivery Liverpool at $14,500/day.

Supramax remained pressured in the US Gulf on limited enquiry while South Atlantic held more stable, with a 66,000 dwt fixed delivery West Africa via South America for redelivery South East Asia at $17,000/day plus a $500,000 ballast bonus.

Handysize stayed soft as the Continent and Mediterranean remained subdued and the South Atlantic and US Gulf weakened on bunker price swings, with a 34,000 dwt fixed US Gulf to East Coast Mexico at around $15,000/day.

Dry Pacific Analysis – Week 11 2026

Capesize closed firmer as miner enquiry returned, with C5 West Australia to China moving into the low $11s per ton and a 181,000 dwt fixed Port Hedland to Qingdao at $10.90/ton.

Panamax activity stayed muted with North Pacific offering relative support, with an 82,300 dwt fixed delivery Rizhao for a trip via NoPac with redelivery Singapore Japan at $20,000/day.

Supramax sentiment stayed soft with demand mainly from the North, with a 55,000 dwt fixed open North China via NoPac to South Korea at $14,650/day.

Handysize fixing remained generally quiet with limited cargo volumes, with a 42,000 dwt open South Korea fixed via Japan to Malaysia at around $13,500/day.

VLCC remained softer w o w but still elevated, with TD15 West Africa to China firming to $127,500/day while US Gulf activity provided support.

Suezmax moved higher, with TD20 West Africa to Continent firming to $212,200/day and TD27 Guyana to UK Continent rising to $232,000/day as the Americas led.

Aframax extended gains, with TD25 US Gulf to Continent at $239,400/day and TD26 East Coast Mexico to US Gulf at $373,000/day, while TD19 cross Med firmed to $301,100/day on a very short list.

LR firmed, with TC20 ME Gulf to UK Continent rising to $81,500/day despite limited fresh Gulf loadings.

MR was firmer overall, with TC21 US Gulf to Caribs easing to $83,400/day while TC2 Continent to US Atlantic Coast firmed to $32,700/day.

Wet Pacific Analysis – Week 13 2026

VLCC remained constrained by disruption and limited volume, with TD3C ME Gulf to China easing to $348,800/day as visibility on Gulf loadings stayed poor.

Suezmax remained heavily constrained East of Suez, with rates highly sensitive to disruption and VLCC competition for limited available volume.

LR firmed, with TC1 ME Gulf to Japan at $105,900/day and TC5 ME Gulf to Japan at $75,000/day as effective tonnage stayed tight.

MR strengthened in the Pacific, with TC7 Singapore to East Coast Australia rising to $31,100/day while East of Suez held broadly firm on a tight list and limited Australia suitable tonnage.

Sale & Purchase Market Analysis - Week 13 2026

Over the past twelve months, reported secondhand buying by nationality was led by Greece with 204 vessels across sectors, while reported selling by nationality was led by Undisclosed with 132 vessels and China recorded 20 vessels sold. On the buying side, Greece was supported mainly by tankers and containers alongside gas carriers, while China’s reported selling was concentrated in dry bulk with smaller contributions across tankers, containers and gas.

This post provides a high-level view of aluminium supply disruption, Gulf logistics pressure, and current freight market dynamics across segments.

The full Allied QuantumSea Weekly Market Report – Week 13 includes:

· In-depth aluminium market analysis covering Gulf smelter disruption, supply tightness & pricing dynamics

· Detailed assessment of Hormuz-related logistics risk and its impact on dry bulk and container flows

· Segment exposure analysis across Handy, Supramax and broader fleet positioning

· Full dry bulk and tanker earnings tables across all vessel classes

· Atlantic & Pacific route-level freight breakdowns with benchmark fixtures

· Baltic indices, TCE calculations & historical trend comparisons

· Secondhand S&P transactions, buyer–seller positioning & asset value trends

· Recycling activity and scrap pricing indicators

👉 Fill in the form below to subscribe and receive the complete PDF directly in your inbox every week.